BIA Advocacy Update

Association shares results from economic impact study of building in the Fargo-Moorhead area

In a study commissioned by the BIA-RRV, the National Association of Home Builders economic team studied the local economic impact of building in the Fargo-Moorhead MSA region. Based off numbers from 2023, they reviewed 663 single-family and 1,066 multifamily housing units built in the Fargo metro area.

Impacts from those units in the first year include:

- $39.3 million in tax and other revenue for local governments

- $2.4 million in current expenditures by local government to provide public services to the net new households at current levels

- $17.7 million in capital investment for new structures and equipment undertaken by local governments

The analysis assumes that local governments finance the capital investment by borrowing at the current municipal bond rate of 4.11 percent.

In a typical year after the first, the single-family and multifamily units result in:

- $17.3 million in tax and other revenue for local governments

- $4.8 million in local government expenditures to continue providing services at current levels

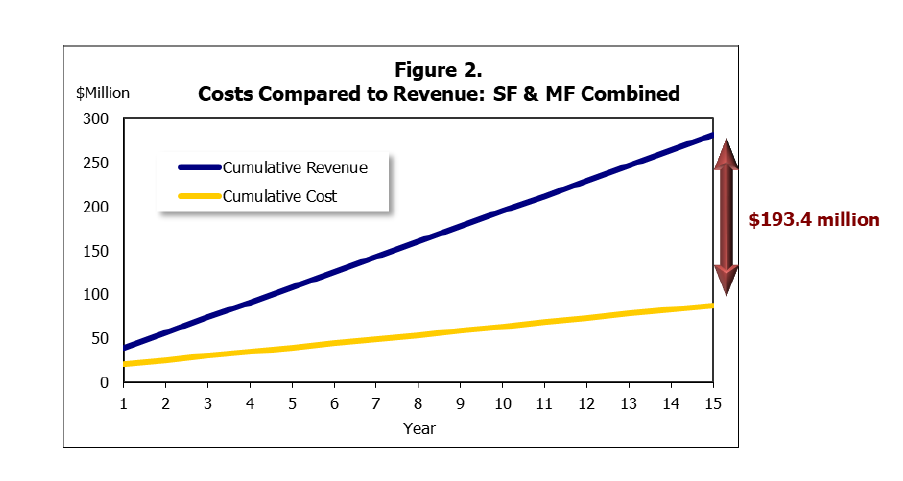

The difference between government revenue and current expenditures is defined as an “operating surplus.” In this case, the operating surplus generated during the first year is large enough to service and pay off all debt incurred by investing in structures and equipment at the start of the first year by the end of the first year. After that, future operating surpluses will be available to finance other projects or reduce taxes. After 15 years, the homes will generate a cumulative $281.1 million in revenue compared to $87.7 million in costs, including annual current expenses, capital investment and interest on debt. See the graph below that illustrates this.

If interested in reviewing the full study, please contact Elizabeth Kosel, 701-232-5846.

North Dakota Association of Builders' leadership visits N.D. Capitol

BIA-RRV leadership and NDAB leadership were working in Bismarck, N.D. on your behalf the first week of February.

They:

- Participated in a joint legislative social with the North Dakota Association of REALTORS which fostered meaningful conversations with state legislators.

- Met with N.D. Attorney General Drew Wrigley to discuss the HUD and USDA rule requiring new homes financed with FHA and USDA mortgages to be built to the 2021 International Energy Conservation Code. North Dakota will be among the hardest-hit states due to the difference between current state standards and the federal mandate. The cost assumptions that the Biden Administration relied on are inaccurate. HUD estimated a cost increase of more than $7,000, which is significant. However, builders are reporting much higher numbers, exceeding $30,000 in some cases.

- We encouraged Attorney General Wrigley to consider joining the multi-state litigation attempting to stop this from taking effect. https://www.nahb.org/news-and-economics/press-releases/2025/01/nahb-15-state-attorneys-general-file-suit-against-huds-energy-codes-mandate.

- Met with Chris Schilken, Commerce Commissioner who provided an overview of the Governor's housing plan.

BIA-RRV directors pictured above, back row, fourth from the left: Shelly Zeis; third from the right: Shannon Roers Jones; second from the right: Adam Olson.

Builders Association of Minnesota Files Federal Injunction to Halt Implementation of Misclassification Bill

On Feb. 13, BAM, the Minnesota Chapter of Associated Builders and Contractors, and commercial construction company J&M Consulting filed their complaint in the US District Court for the District of Minnesota regarding worker misclassification.

Read BAM's release here.

Set to begin March 1, the ruling expands the Dept. of Labor and Industry's authority and begins a new 14-pt test.

They are seeking a preliminary injunction to immediately halt the implementation of the bill while the court considers the merits of the case.

1. was established and maintained separately from and independently of the person for whom the services were provided or performed;

2. owns, rents, or leases equipment, tools, vehicles, materials, supplies, office space, or other facilities that are used by the business entity to provide or perform building construction or improvement services;

3. provides or performs, or offers to provide or perform, the same or similar building construction or improvement services for multiple persons or the general public;

4. is in compliance with all of the following:

(i) holds a federal employer identification number if required by federal law;

(ii) holds a Minnesota tax identification number if required by Minnesota law;

(iii) has received and retained 1099 forms for income received for building construction or improvement services provided or performed, if required by Minnesota or federal law;

(iv) has filed business or self-employment income tax returns, including estimated tax filings, with the federal Internal Revenue Service and the Department of Revenue, as the business entity or as a self-employed individual reporting income earned, for providing or performing building construction or improvement services, if any, in the previous 12 months; and

(v) has completed and provided a W-9 federal income tax form to the person for whom the services were provided or performed if required by federal law;

5. is in good standing as defined by section 5.26, if applicable;

6. has a Minnesota unemployment insurance account if required by chapter 268;

7. has obtained required workers' compensation insurance coverage if required by chapter 176;

8. holds current business licenses, registrations, and certifications if required by chapter 326B and sections 327.31 to 327.36;

9. is operating under a written contract to provide or perform the specific services for the person that:

(i) is signed and dated by both an authorized representative of the business entity and of the person for whom the services are being provided or performed;

(ii) is fully executed no later than 30 days after the date work commences;

(iii) identifies the specific services to be provided or performed under the contract;

(iv) provides for compensation from the person for the services provided or performed under the contract on a commission or per-job or competitive bid basis and not on any other basis; and

(v) the requirements of item (ii) shall not apply to change orders.

10. submits invoices and receives payments for completion of the specific services provided or performed under the written proposal, contract, or change order in the name of the business entity. Payments made in cash do not meet this requirement;

11. the terms of the written proposal, contract, or change order provide the business entity control over the means of providing or performing the specific services, and the business entity in fact controls the provision or performance of the specific services;

12. incurs the main expenses and costs related to providing or performing the specific services under the written proposal, contract, or change order;

13. is responsible for the completion of the specific services to be provided or performed under the written proposal, contract, or change order and is responsible, as provided under the written proposal, contract, or change order, for failure to complete the specific services; and

14. may realize additional profit or suffer a loss, if costs and expenses to provide or perform the specific services under the written proposal, contract, or change order are less than or greater than the compensation provided under the written proposal, contract, or change order.

For more information, click here.

Powered By GrowthZone